IMPORTANT UPDATE: Chief treasury secretary Steve Barclay announced on 17th March 2020 that the introduction of the new IR35 private sector reforms will be delayed by twelve months from 6th April 2020 to 6th April 2021 as a result of the COVID-19 pandemic. The article below has been updated to reflect this. For more information about the delay, visit the HMRC website.

Have you ever wondered what determines someone as an employee rather than a contractor? With changes to IR35 legislation due to hit the private sector from April 2021, it is very much in your interest to find out.

There has been quite a lot in the news recently about the classification of individuals when it comes to their working arrangements. Whether medical professionals, broadcasters, taxi or fast food delivery drivers, there seems to be more confusion than ever as to whether someone is classified as an employee, worker, contractor or self-employed for the purpose of wage and benefit entitlements and how they are taxed.

With changes afoot, we explain what IR35 is, whether it is something you should be preparing for and how we can help.

Glossary

For the purpose of this article, the following definitions apply:

- Contractor – An entity (often an individual) that undertakes a contract to perform a service or job.

- Disguised employment – Where contractors provide their services to a business via an intermediary, such as a PSC rather than directly as an employee.

- Engager/Customer/Client – The business receiving the services of the contractor.

- Fee-payer – The organisation that pays the PSC for work performed.

- Intermediary – an organisation, such as a PSC, that acts as an agent between the individual providing a service and the customer that receives it.

- Personal Service Company (PSC) – a company owner-managed usually by a sole Director or a few family members.

What is IR35?

IR35 is the common term given to anti-tax-avoidance legislation specifically designed to tax ‘disguised employment’.

Its purpose is to prevent an individual, who under ordinary circumstances would be viewed as an employee, from benefiting financially by offering their services as a contractor through an intermediary, usually a PSC or sometimes a Limited Liability Partnership (LLP), in order to avoid PAYE.

It is generally accepted that going it alone in business is riskier than being an employee due to no guarantees of a regular income and no access to employment benefits. As a result, contractors are provided greater tax advantages than their employed counterparts.

However, it has not been lost on HMRC that many contractors have exploited these rules so that they can receive both a guaranteed source of income (as if an employee) whilst also benefiting from the tax breaks that come from having a PSC.

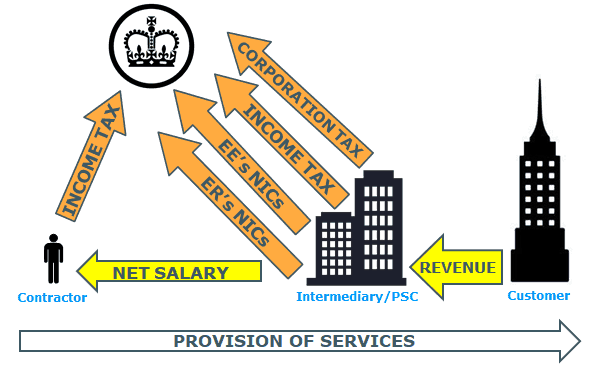

IR35 legislation seeks to counter this unfair exploitation by taxing contractors as if they were employees. This means in simple terms, for example, that a contractor’s PSC would receive payments for its contractor’s services net of PAYE instead of having all its gross income subjected solely to Corporation Tax (CT) as if it was turnover.

Below you can see how being caught within IR35 works in practice:

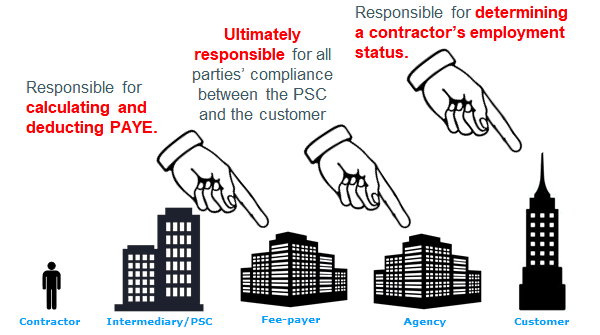

An Important Distinction

It is important to state that the IR35 rules only apply to PSCs (also LLPs in some circumstances).

As such, any individual providing a service as a self-employed business such as a sole-trader or partnership (i.e. not a company) need not be concerned by the IR35 rules or the upcoming changes to them.

Instead their engager, who is ultimately responsible, should consider whether the individual should be classified as an employee, worker or self-employed when considering their employment status.

More information on the distinction between an employee, worker and the self-employed can be found here.

The Problem with Employment

It shouldn’t come as a surprise that HMRC introduced the IR35 rules given that they are losing out on employers’ National Insurance Contributions (NICs) as a result of businesses choosing to hire contractors instead of employees.

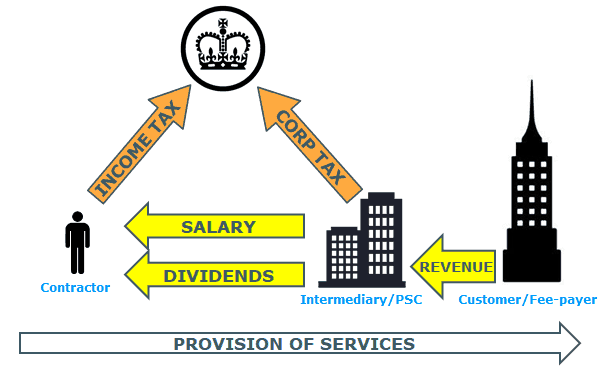

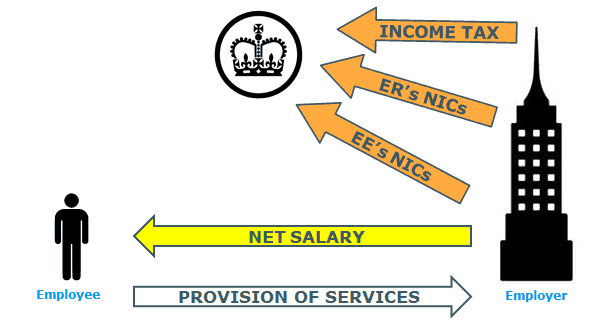

The diagrams below show how disguised employment operates in practice compared to a normal employer/employee arrangement:

Unfortunately for HMRC, contractors can prove to be more desirable to hiring businesses than employees due to the additional demands that come with them including:

- Suffering Employer’s NICs (13.8% of an employee’s salary above £8,632)

- Having to offer and contribute to a Workplace Pension (3% of an employee’s salary if above £6,136)

- Having to offer obligatory employee benefits (e.g. sick pay, holiday pay)

- Having to offer additional benefits to help attract the best talent

- Spending time and resources complying with employment law

As a result, businesses have instead turned to contractors to reduce the burden of hiring employees, whilst still benefiting from a service like that received from a member of staff.

As far as contractors are concerned, it is often recognised as more tax-efficient for them to provide their services via an intermediary, such as a PSC, for the following reasons:

- Their income is subjected to CT at 19% after deduction of expenses (rather than 20/40/45% Income Tax [IT] on salary)

- Extraction of company profits via dividends is subjected to 7.5% IT over £2,000 (rather than 12% Employee NICs on salary above £8,632)

- Directors are not subjected to minimum wage rules and can therefore pay themselves a salary that ensures no IT or NICs arise

It is inevitable therefore that both engagers and contractors usually prefer conducting business under this arrangement rather than under an employer/employee relationship.

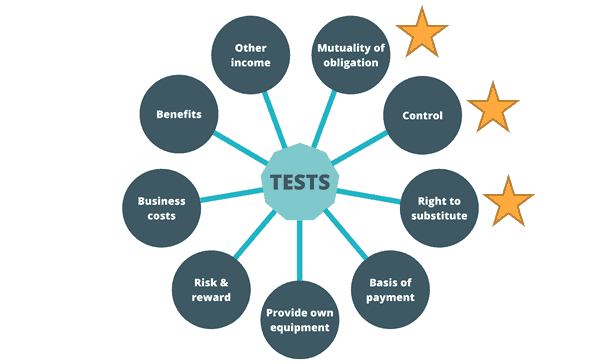

Determining an Individual’s Employment Status

There are various factors that help determine a contractor’s working status. Such factors include, but are not limited to, the following:

- Whether there is mutuality of obligation (i.e. the customer is obliged to provide work and pay for it whilst the contractor is also obliged to undertake the work)

- The way in which the work undertaken is controlled and who by

- When the work is performed by the contractor and for how long

- Whether the work performed is an integral part of the customer’s business or merely an additional service

- Whether there is a risk to the contractor of not being paid a regular remuneration

- Whether the equipment used belongs to the contractor or the engager

- Whether the contractor has the right to receive holiday pay, benefits etc

- The number of income sources the contractor has (i.e. they are not solely reliant on one customer)

- Whether a substitute could be sent to fulfill any contract obligations

- Whether the engager or contractor suffer relevant business costs

Depending on the answers to each of the points above, any particular contract arrangement will be determined as either “inside IR35” or “outside IR35”.

HMRC’s previous tax tribunal cases have intimated the three most significant factors to consider when determining the existence of disguised employment. These can be seen in the wheel above.

HMRC’s Check Employment Status for Tax (CEST) Tool

Originally created in March 2017 the tool, which can be accessed here, has been designed by HMRC to help engagers determine the IR35 status of the contractors it uses.

It is a free, online questionnaire, the result of which HMRC claim they will stand by in the event of an enquiry or investigation so long as the information that has been entered can be proven to be true. The result alone, therefore, does not constitute sufficient evidence and should be used for guidance only.

Originally, CEST was heavily criticised from all sides for being too simplistic and was seldom trusted since it resulted in the NHS being landed with a £4.3m tax bill.

Despite NHS Digital using CEST on a case-by-case basis to determine the employment status of each of its contractors, the tool’s numerous flaws and inaccuracies led to HMRC concluding that many of the organisation’s contractors were in fact inside IR35 when CEST had determined otherwise.

Fortunately, since this debacle, HMRC have made wholesale improvements to the tool, although we would still encourage engagers and contractors alike to seek an independent review from IR35 experts such as ourselves.

For details about our IR35 contract review service, simply click here.

“Outside IR35”

If, having gone through the above tests, a contractor is deemed to be “outside IR35”, this means that they are considered not to be a disguised employee and may, therefore, continue offering their services to the engager in the same manner.

CASE STUDY: Kickabout Productions Ltd Vs HMRC (2019)

Talksport radio show host, Paul Hawksbee, who owns Kickabout Productions Ltd argued that without his PSC he would be classified as self-employed for the services he provides Talksport with.

His arguments included:

- He had total freedom to decide the content and format of each show as well as the guests that appeared on it

- Any breaking news stories that occurred would only be covered if he felt they would be relevant, interesting or important to the show

- He did not commit to many functions/activities of Talksport, including their social media accounts, and had no obligation to do so

- Talksport was under no obligation to provide him with any work

- He had no rights to receive holiday or sick pay, a pension or paternity leave

- He could arrive at the studio at any time prior to the show

- He did not attend any post-show de-briefings and was not subject to any appraisals

The Lower-Tier Tribunal judge ultimately ruled in favour of Kickabout Productions Ltd based on the arguments provided above, however the conclusion reached was only because the jury could not determine which way to decide, forcing the judge to use their casting vote.

“Inside IR35”

If a contractor is deemed to be “inside IR35”, meaning that they are found to be a “disguised employee”, the fee-payer of that worker, whether the agency or the engager, must deduct PAYE from the individual, even if the worker continues to provide services via their own PSC.

CASE STUDY: Christa Ackroyd Media Ltd Vs HMRC (2017)

Christa Ackroyd, known best as the former TV presenter for BBC’s regional news programme, “Look North”, was contracted by the BBC via her PSC, Christa Ackroyd Media Ltd (CAM Ltd). She also argued she would be classed as self-employed if her company did not exist.

The main points of the case were:

- The BBC entered a 7-year contract with CAM Ltd for the services of Ms Ackroyd, paying a monthly fee for which they received first call on her services

- The company’s income from other sources was relatively low

- Ms Ackroyd could request and arrange interviews as well as make suggestions to improve “Look North”

- She was not contractually bound by the BBC’s Editorial Guidelines, although did have an obligation to comply with them as the BBC had editorial responsibility for “Look North”

- Ms Ackroyd had no desk at the BBC, used her own phone and computer and had no set working hours (other than presenting the programme)

- She had no entitlement to sick pay, holiday pay or any other employment rights

- She was unable to provide a substitute and was forbidden to provide other TV or radio services in the UK without the consent of the BBC

The Lower-Tier Tribunal determined that there was mutuality of obligation between Ms Ackroyd and the BBC and that they exerted sufficient control over her work. Furthermore, they concluded that factors such as the length of the contract and the protection of Ms Ackroyd from financial loss supported a hypothetical contract of employment and therefore found in favour of HMRC. The decision was upheld by the Upper-Tier Tribunal on appeal and is thought to have cost Ms Ackroyd £420,000 in unpaid taxes.

The Financial Consequences of IR35

If, like Christa Ackroyd, a contractor is found to be captured within the IR35 legislation they will not only have backdated PAYE to pay across to HMRC but their fee-payer, whether an agency or the engager of their PSC’s services, will have to ensure that these deductions are made for any future service provision.

It goes without saying that this can be very damaging financially to both the customer and the contractor and may force contractors into accepting employment as an individual and/or winding down their PSCs so as to ensure a regular source of income without running the risk of penalties and interest for unpaid taxes.

See below a simple example of how employment as an individual, being captured inside and outside IR35 compare to each other:

Upcoming Changes to IR35 Legislation

- A shift of liability

From 6th April 2021, medium & large-sized engagers operating in the private sector will become responsible for determining the IR35 status of any contractors it chooses to use.

This means that the risk of deciding whether a contractor is deemed to be treated as such for tax purposes has now been taken out of the hands of the PSCs and firmly placed with the customers, leaving contractors naturally concerned that they may soon have to incur PAYE or worse witness the termination of their existing contracts.

The above diagram shows how the fee-payer is responsible for PAYE deductions, whilst the customer is responsible for the contractor’s employment determination. It is worth noting that the client retains the liability even if a recruiter/agency makes an IR35 determination for them.

What constitutes a medium or large-sized engager?

As per the Companies Act 2006, a medium or large-sized business is defined as such if two of the following three requirements are met:

- It has an aggregate turnover above £10.2m

- It has an aggregate balance sheet total above £6.1m

- It has more than 50 employees

Furthermore, if the customer is defined as medium or large prior to 6th April 2021, they must apply the new rules immediately when they come into effect.

Also note that all subsidiaries, regardless of their individual size or location, will be classified as medium or large engagers if the combined size of all businesses within their group meets the criteria above.

If a customer does not meet the above criteria, the responsibility of a contractor’s IR35 status remains with the contractor themselves.

- The introduction of a ‘Client-Led Status Disagreement Process’

In the event of a disagreement between the engager and the contractor over their IR35 status, the contractor can bring an official challenge to the customer. Such a challenge must be responded to within 45 days outlining the decision and the reasoning behind it with the provision of evidence to back-up the determination otherwise customer will be held responsible for the deduction of PAYE.

While it is usually in the interest for engagers to determine contractors as sitting outside IR35, some may still feel that the risk is too great and, unfortunately for contractors, the end-client’s opinion is effectively final.

Furthermore, contractors’ current routes of appeal such as an Alternative Dispute Resolution (ADR) or appeal to a tax-tribunal may be shut off by this new process, as any dispute would be between the customer and the contractor as opposed to HMRC.

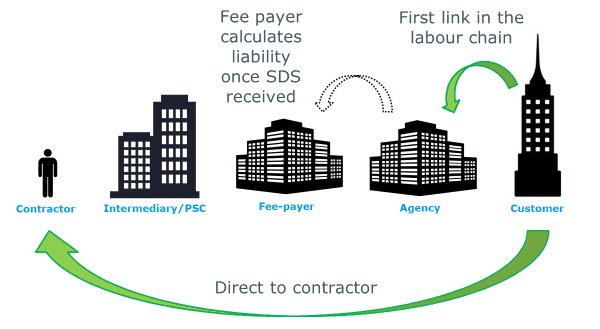

- The introduction of ‘Status Determination Statements’

In a bid by HMRC to increase transparency, engagers will be required to provide a ‘Status Determination Statement’ (SDS) to both the contractor directly and the next party in the labour supply chain until it reaches the fee-payer. The SDS must include both the status decision that was made as well as the reasoning behind it.

Until an SDS is issued, the customer will be deemed the fee-payer and therefore liable. The illustration below shows how the SDS should be issued:

Overseas Scenarios

Frustratingly, at time of writing, it is not entirely clear what the rules will be it when it comes to scenarios involving overseas parties, however this is what we anticipate:

Where there is no agency acting as a middleman between the PSC and their client, it is the responsibility of the contractor, as the only UK-based organisation, to decide their own IR35 status. The customer will still be responsible as the fee-payer to deduct PAYE.

Where there is a UK-based agency arranging work for the PSC, it is they who will be liable to deduct PAYE. However, it remains the customer’s responsibility to determine the IR35 status of the contractor.

Where services are provided abroad by a UK-based contractor, the IR35 rules will only apply if the contractor (individual) is deemed a UK resident for tax purposes.

HMRC’s guidance public sector guidance says that “where an intermediary is outside the UK, but the worker performs services in the UK, fee payers must still deduct tax”.

In short, if there is a UK liability arising as a result of the working arrangement, IR35 will apply regardless of where the parties are based.

What Should I Do to Prepare?

Contractors – it is important to initiate dialogue with your fee-payer and/or customer to learn of their plans regarding IR35 and how they intend to assess and remunerate you from 6th April. By asking the questions now, you give

yourself time to make alternative arrangements where necessary to ensure your income is protected.

It makes sense for you to review, and potentially tweak, the way you work if you are concerned you might be caught inside IR35. It is also important that your service contract reflects the working relationship you have with your customer and this will also need to reinforce that you are not caught within IR35.

Our IR35 contract review service can help you with this.

Engagers – you need to determine how you are going to assess your contractors before the 6th April deadline.

A blanket-assessment will likely save time and money in the short-term; however, it will likely result in either:

- Contractors being caught inside IR35, resulting in the need to either employ them or lose their services, both of which have financial implications

- Contractors being deemed outside IR35, resulting in running the risk of misclassification and facing penalties from HMRC

- HMRC deeming you liable as blanket assessments have been confirmed as non-compliant with IR35 rules

Given that none of the above outcomes are particularly appealing, we would suggest that contractors are assessed on a case-by-case basis using an independent expert such as ourselves to ascertain and reinforce the correct classification.

Doing so will allow you to benefit from the flexibility and savings provided by contractors whilst also protecting you against HMRC penalties for those who sit within IR35.

Frequently Asked Questions

Q. Why does IR35 sound familiar?

A. The legislation itself has been around nearly 20 years, although the public sector underwent similar changes in April 2017 to those about to be brought into the private sector.

Q. My PSC has been determined as being caught inside IR35 and will be paid after 6th April 2021 for work I performed before this date; should this income be subjected to PAYE?

A. Yes. The rules apply to all payments made on or after 6th April 2021 regardless of when the work was performed. Your fee-payer will, therefore, be responsible for deducting this from you.

Q. Am I entitled to employment benefits if my PSC is caught within IR35?

A. No. The IR35 legislation only dictates how a contractor inside IR35 should be taxed. Therefore, there is no obligation for a customer to provide holiday entitlement or a workplace pension for example.

Q. What if I have several contractors providing their services with identical Terms & Conditions? Can I blanket assess these to save time?

A. Yes. HMRC has confirmed that it is acceptable to do this, although any enquiry by HMRC may consider the contractors individually so it is important to be certain that all contractors are identical in this regard to avoid misclassification.

Q. Does this legislation apply to umbrella company workers or employees?

A. No

Q. Will HMRC investigate a contractor’s prior years’ IR35 status if their engager changes it?

A. HMRC have said that they won’t, although they most certainly can. In short, only they know the resources available to them and the number of enquiries they are able/wish to make. We would, therefore, recommend that Aston Shaw clients take out our tax investigation cover to ensure they are not charged for time spent defending them against any IR35 enquiry.

Q. Can contractors combine forces to avoid the new rules?

A. In short, no. A company will still be defined as a PSC if a worker (or family member) control more than 5% of the shareholding of that company, are entitled to more than 5% of the dividends of that company or are remunerated in benefits or other means.

Q. I’ve heard about this tax avoidance scheme…?

A. Our opinion: Steer clear.

If HMRC isn’t paying attention to a given scheme now, they probably will do in the future often with devastating financial consequences to those who were involved. Remember, if it sounds too good to be true, it almost certainly is.

Q. Are charities or trade organisation affected?

A. Yes

Q. What is the fee-payer responsible for deducting?

A. Purely the PAYE that occur as a result of the IR35 liability calculation.

The fee payer is not responsible for deducting statutory payments, student loan repayments, pension contributions or holiday pay.

Q. What is the trigger point for the new IR35 rules? Is it:

– the date of the service provided or

– the date of the invoice for the services provided or

– when payment is made for the services provided?

A. As per HMRC, it applies to payments for services provided on or after:

– the date that the engager ceases to be classified as a small business or

– 6th April 2021 if the customer is already classified as a medium or large business.

Q. How does IR35 interact with the Construction Industry Scheme (CIS)?

A. IR35 overrides CIS so there will still be an expectation on the construction industry to properly assess their workforce.

Q. Does a contractor qualify for employment benefits if they are caught “inside IR35”?

A. No. The contractor’s entitlement to any employment benefits will arise from the relationship they have with their own PSC. For example, if the contractor receives a salary from their PSC then employment benefits will be available.

Q. Can a customer create a new company to get around the IR35 rules?

A. Unlikely as the connected person rules apply to IR35. The aggregate of the turnover of all businesses owned by…

- The individual

- The individual’s spouse or civil partner

- A relative of the individual

- the spouse or civil partner of a relative of the individual

- A relative of the individual’s spouse or civil partner

- The spouse or civil partner of a relative of the individual’s spouse or civil partner.

…must be considered when determining whether the engager is a small or medium business.