The Domestic Reverse Charge (DRC) is a major change to the way in which VAT is collected in the construction industry and will come into effect from 1st March 2021.

Why has it been introduced?

The Domestic Reverse Charge has been introduced by HMRC to combat fraud, in particular, missing trader fraud which costs the UK an estimated £100m per year.

Missing trader fraud usually occurs where UK-VAT registered labour suppliers provide staff to a contractor but then ‘disappear’ without paying HMRC the VAT they have charged. The contractor then reclaims their element of the VAT from HMRC leaving the Revenue out of pocket.

The fraudulent organisation may then reinvent itself with a different name and structure, making it difficult for HMRC to identify and recoup any old VAT debt.

Furthermore, with no intention of paying any VAT to HMRC, labour suppliers are able to offer heavily discounted rates to ensure they secure contracts, negatively impacting those businesses who abide by the rules.

How does the Domestic Reverse Charge work?

UK VAT-registered customers receiving a service reported under the Construction Industry Scheme (CIS) that is subject to VAT (i.e. at 5% or 20%) and who make onward supplies of the same building and construction services supplied to them, will have to pay any VAT charged to them to HMRC instead of paying the supplier.

By removing the need to pay VAT within the supply chain, there is nothing to defraud which should, in theory at least, reduce the amount lost by HMRC.

What services are affected?

CIS services affected by the DRC are as follows:

- Constructing, altering, repairing, extending, demolishing or dismantling buildings or structures (whether permanent or not), including offshore installation services

- Constructing, altering, repairing, extending, demolishing of any works forming, or planned to form, part of the land, including (in particular) walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours

- Pipelines, reservoirs, water mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence

- Installing heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems in any building or structure

- Internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration

- Painting or decorating the inside or the external surfaces of any building or structure

- Services which form an integral part of, or are part of the preparation or completion of the services described above – including site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works

What is NOT a CIS service?

CIS services not affected by the DRC are as follows:

- Drilling for, or extracting, oil or natural gas

- Extracting minerals (using underground or surface working) and tunnelling, boring, or construction of underground works, for this purpose

- Manufacturing building or engineering components or equipment, materials, plant or machinery, or delivering any of these to site

- Manufacturing components for heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems, or delivering any of these to site

- The professional work of architects or surveyors, or of building, engineering, interior or exterior decoration and landscape consultants

- Making, installing and repairing art works such as sculptures, murals and other items that are purely artistic

- Signwriting and erecting, installing and repairing signboards and advertisements

- Installing seating, blinds and shutters

- Installing security systems, including burglar alarms, closed-circuit television and public address systems

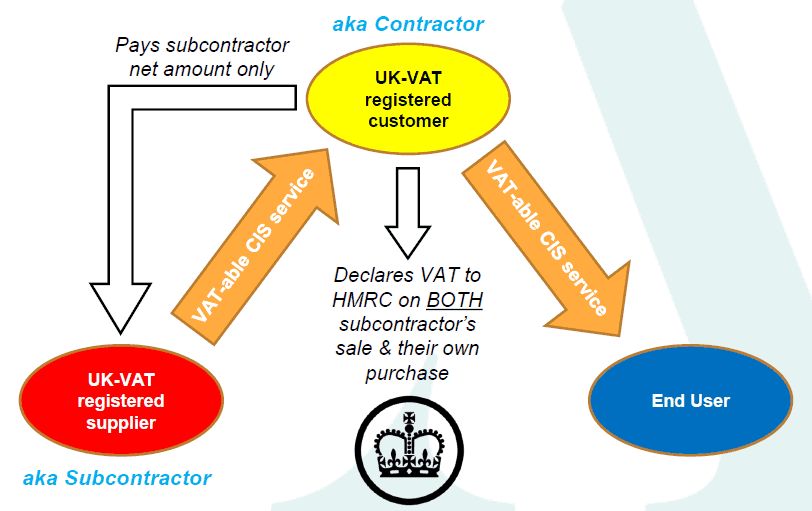

The Domestic Reverse Charge in practice

As per the diagram above, rather than the contractor paying the subcontractor VAT on the services it receives, it instead pays the subcontractor net of VAT and declares on its own VAT Return both the VAT on the subcontractor’s sale as well as its own purchase.

How will this affect my business?

Subcontractors – They will not receive any VAT from the contractor which will negatively affect their cash flow position but on the other hand will mean that their VAT liability to HMRC will be reduced as the contractor is now responsible for paying the VAT to HMRC.

Contractors – They will not have to pay the subcontractor any VAT which will positively affect their cash flow position but on the other hand will mean that their VAT liability to HMRC will be increased as the subcontractor is no longer responsible for paying the VAT to HMRC.

Neither the subcontractor or contractor are financially better or worse off as a result of the DRC although what is clear is that it will have a significant impact on the cash flow of all businesses in the supply chain where the DRC applies.

What is an ‘End User’?

Simply put, an End User is an entity that does not make onward supplies of the CIS services it receives. When this is the case, the DRC should not apply when selling to an End User:

As from the diagram above the End User, Mrs Jones, in this case, has no intention of on-selling the CIS service provided to her and as a result must pay VAT to Construction Co. Ltd in the normal way.

The transaction between the subcontractor and contractor, however, has not changed and therefore the DRC still applies, with the contractor taking full responsibility for the declaration of the VAT.

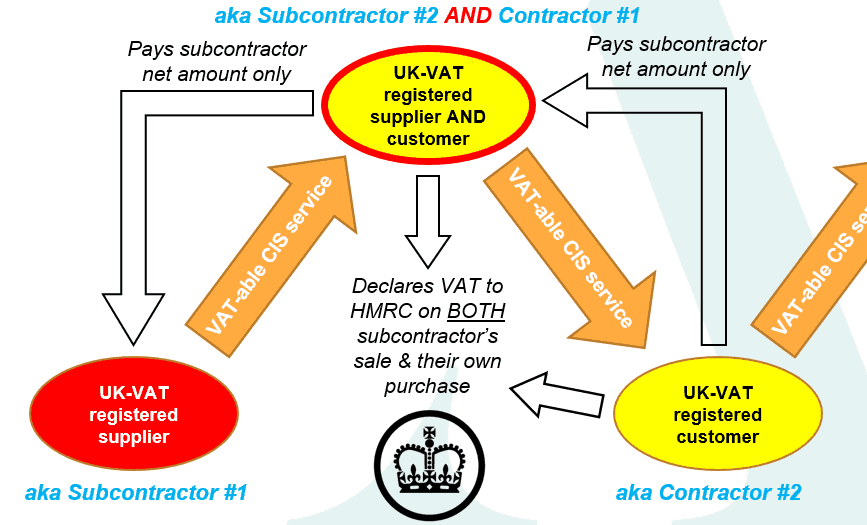

What if there is no immediate End User?

In the situation where there is an onward supply of CIS services by more than one entity, the DRC continues to apply until the End User is identified. This means that some contractors will become a subcontractor also and must take care to ensure they apply the DRC correctly when invoicing for their CIS services.

What about the provision of mixed goods and services?

The sale of all goods and certain services do not qualify for the DRC when billed for on their own but when coupled with any service that is subject to the DRC, the DRC should be applied to all products and services in that supply.

For example, Bob the Builder constructs a staircase off-site before selling it to and installing it for his contractor. Even though the only good or service that would qualify for the DRC if provided separately would be the staircase installation, because all the services have been provided together the DRC will apply to all of them.

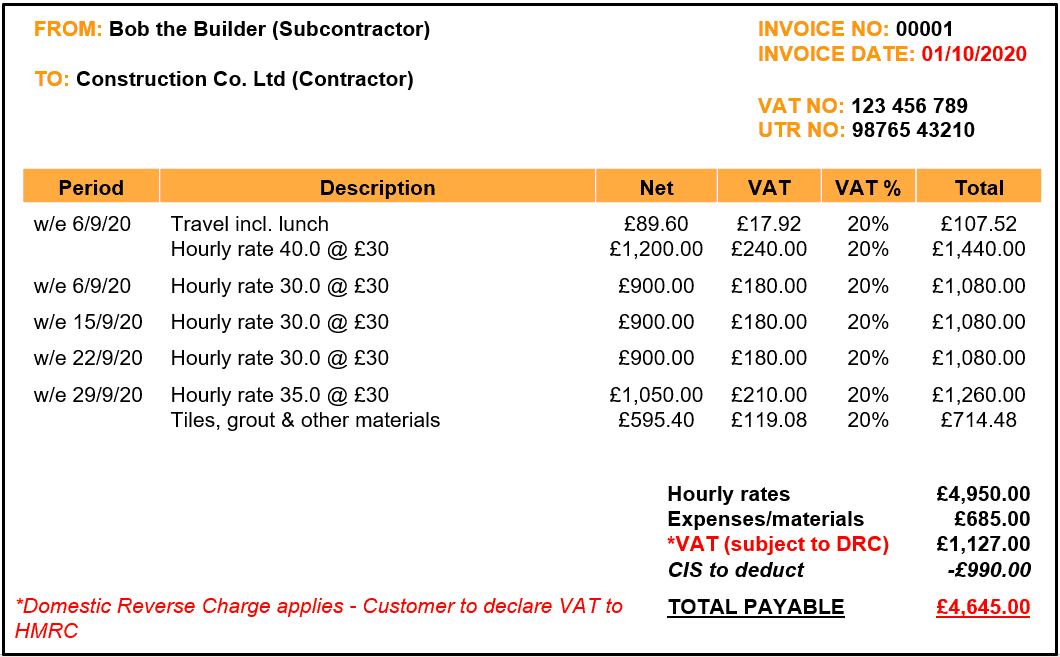

How do I account for the DRC on my invoice?

There are many methods and facets of billing for work including single payment contracts, self-billing invoices, authentication receipts, retention payments and periodic payment contracts so for this example we’ll use a simple subcontractor invoice for a month’s worth of work renovating a bathroom:

The aspects of the invoice above to take particular notice of are highlighted in red.

Firstly, the tax point for VAT purposes, which in this case is the date of the invoice, is on or after 1st March 2021, therefore, the DRC needs to be applied.

Secondly, it needs to be clear that the VAT due on the goods and services provided is shown as being subject to the DRC and that it is the customer’s responsibility to declare this to HMRC.

Finally, the amount payable to the subcontractor needs to exclude the VAT stated on the invoice, which in the above example equates to the hourly rates worked plus expenses/materials minus any CIS required to be deducted. The amount of VAT can be recorded in isolation on the invoice if this makes it easier for the customer to understand what is due.

How you should prepare for the Domestic Reverse Charge

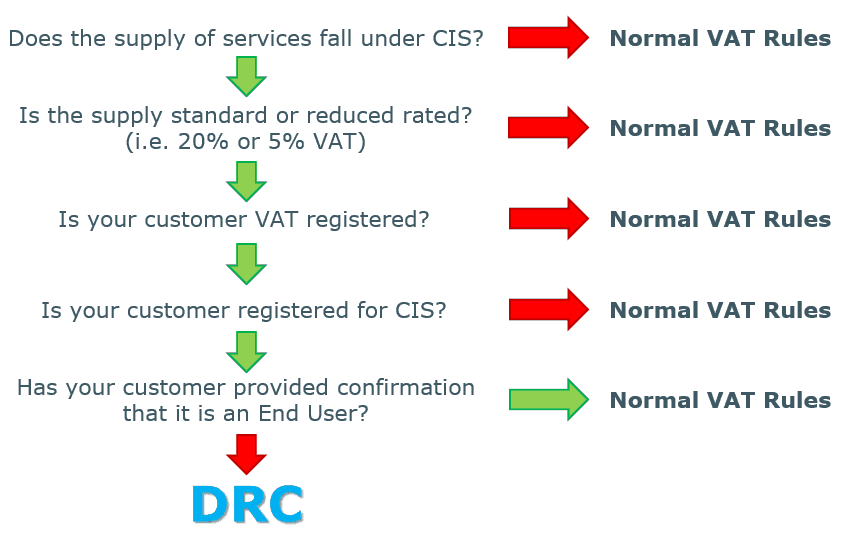

1. Check whether the DRC will affect your sales, purchases or both and communicate your position with your customers and suppliers.

Suppliers can determine whether the DRC applies to their suppliers by using the following flow chart. To avoid any confusion a green arrow represents “yes” while a red arrow represents “no”.

For sole-traders

- Individual’s name

- UTR number

- NI number

For partners

- Partnership name

- Partner’s name

- Partnership UTR number

- Partner’s UTR or NI number

For companies

- Company name

- Company UTR number

- Company registration number

Once you know which of the entities in your supply chain are affected by the DRC, it is important to communicate how the DRC will apply when dealing with you so that both parties are aware what is expected of them when doing business.

Subcontractors – Include a statement in your own terms and conditions to say that you will assume that your customer is an End User unless they confirm they are not.

Contractors – Make it clear in writing when necessary that you are not an End User to ensure that the DRC is being applied.

2. Make sure your invoicing and bookkeeping systems are ready for the new rules and ensure all your relevant staff are educated on how and when to apply the DRC

Cloud accounting software providers such as Xero, QuickBooks Online and Sage all said that they would be ready for the original 1st October 2019 deadline (before it was postponed), therefore we anticipate that they will also be ready for March 2021.

However, despite the delay, there are still some software providers who will not update their systems to be ready for the DRC, therefore you may need to contact your software provider for advice on how to record any affected transactions correctly when the deadline nears.

If you use a bookkeeping method that will not automatically compile your VAT Return for you, then you will need to do the following for your DRC transactions:

Suppliers

- Enter the net value of your sale (i.e. ex-VAT) in Box 6

Contractors

- Enter the VAT on the supplier’s sale in Box 1 (this would normally be done by the supplier)

- Enter the VAT on your purchase in Box 4

- Enter the net value of your purchase in Box 7

3. Calculate how your cash flow will be affected and take the necessary steps to prepare

Contractors – You will find that you retain more cash than normal by withholding VAT from your suppliers but be wary that this is not your money as it will need to be paid to HMRC as per your next VAT Return.

Subcontractors – You will find that you have less cash than normal due to your customers paying the VAT on your affected sales but this will result in a lower VAT liability to HMRC after preparing your next VAT Return. You may even start to receive VAT refunds from HMRC in which case you might want to switch from quarterly to monthly VAT returns to receive repayments faster.

Frequently Asked Questions

- Who is liable for the VAT of the supplier’s sale subject to the DRC if the customer goes bust?

- Still the customer

- Are VAT error corrections dealt with in the same way?

- Yes, if the error is <£10,000 the following VAT Return can be adjusted

- What are the penalties for failing to comply?

- HMRC have stated that they will apply a light touch for the first six months following the DRC’s introduction and that penalties will only be considered if businesses are deliberately taking advantage of the new rules by not implementing it correctly.

- What does “Domestic” in Domestic Reverse Charge mean?

- UK – This is to ensure it distinguishes itself from the already existing Reverse Charge procedure that is in place for B2B transactions that occur between businesses in different EU member states.

If you would like to discuss the Domestic Reverse Charge with one of our experts, then please contact us.